August

06

August

06

The Blow Off Top Begins

An impressive jobs report took stocks to new all time highs on Friday as the Bureau of Labor Statistics showed a gain of 255k jobs versus estimates of 180k. More importantly wage growth was a tick better than expected coming in at 2.6%. This positive report comes after a disappointing 2nd quarter GDP number and misses on ISM sentiment indicators. Overall US data is mixed, but has been averaging upside surprises for the last 6 weeks. Markets now turn their attention towards the Jackson Hole symposium hosted by the Federal Reserve on August 25th-27th.

Taking a closer look at stocks, nothing has been happening prior to Friday’s bullish breakout. Stocks moved sideways in a range of less than 1% for three weeks straight, with volume and volatility plunging to remarkable lows. The S&P 500 SPDR ETF SPY saw an average volume of 66 million shares over the period from July 18th to August 5th, versus a 3 month average volume of 95.2 million. Spot VIX has fallen to 11.39 as of Friday’s close, setting a new low for the last three weeks. Bonds and FX have also been mostly silent as the Dollar index has been range bound between 95 and 97, while the US 10 year bond yield is stuck within 1.47% and 1.57% after the June move off the 1.33% YTD low.

S&P 500 SPDR ETF (SPY), White Line on Volume is 66mm share average for 7/18-8/5

The markets seem stuck in a funk and nothing can break the spell. Starting with Brexit there has been a range of geopolitical and economic events that markets have totally ignored. Each time, the market stabilizes and drifts higher, albeit on lower volume and declining volatility. I threw in the towel on fundamentals and economic data a few months ago as it seems every possible threat is immediately doused in new central bank promises that suppress volatility. The twitchiness of central banks seems to be getting more and more nervous as they now sound on the alarm at the slightest possibility of a risk. Given this picture we must consider that if a top were to occur in these conditions, what exactly would have caused the turn when we look back on it?

What we currently know is that the US labor market is tightening, inflation is accelerating, stocks are setting new highs daily and nobody thinks the Fed will raise rates even once within the next year. Market participants are probably betting that even if the does Fed hike it will only be once. The Fed has lost credibility to the degree that even if a full on normalization of rates becomes required, markets assume they will not pursue that course simply because it would cause too much damage. The trade in this case is to simply keep buying stocks until central banks make it completely clear they will raise rates in a full on old school rate hiking cycle.

The error with this line of reasoning is the assumption the Fed and other central banks actually have to do anything hawkish for stocks to decline dramatically. As the FOMC has backed further away from rate hikes at each meeting this year, investors have relaxed and are waiting for an obvious signal from the Fed that the party is over. There is a general complacency with regards to the extent of short term losses that are possible, this is evident as the VIX falls to new lows on a daily basis. Central banks may be able to create new money to buy bonds or stocks over the medium term, but they cannot instantly arrest a catastrophic decline due to sudden realization that there is a structural lack of liquidity in financial markets due to the crowding out of sell side trading over the last 8 years by central banks and regulatory pressures.

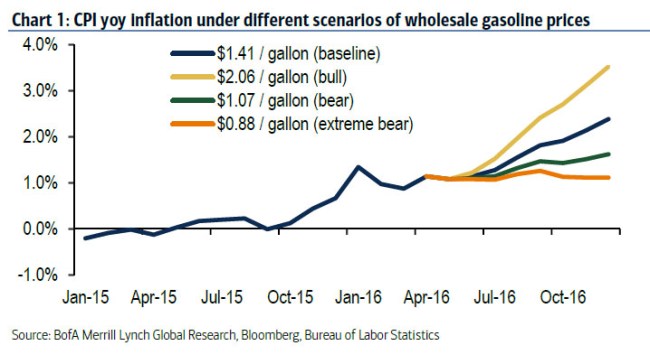

As for what will set off this decline, it could be anything and it could be nothing. All we can monitor is the level of central bank confidence, which will wane as the chasm widens between what inflation data shows and what central banks actually acknowledge relative to their mandate. As the year draws to an end and oil declines roll out of the year over year calculations, inflation will move above target in the United States, United Kingdom, Europe and Japan. Recall that the BOE, BOJ and ECB all use headline inflation as their target which includes energy prices.

BofA: US CPI Under Gasoline Price Scenarios

The moment it becomes clear that the combo of oil, rent and wages will drive inflation to overshoot 2%, confidence in any form of massive central bank stimulus waiting at the rescue will evaporate. All it takes is the idea that a huge increase in QE is untenable due to inflation and the political situation. I do not dispute the idea that central banks would in act in the event of a decline, but can they act before a week long flash crash knocks 40% off stock prices? I doubt it. After the initial stampede from risk, additional QE programs are unlikely to restart the asset bubble again unless the Fed buys stocks directly. Central banks will then have to wait for deflation to set in before starting easing once again, which could take over a year.

As we draw closer to Q1 2017 I am positioning my portfolio of put options against rates sensitive stocks, momentum technology stocks, government bonds with short oil as a hedge. This theory is reliant on oil not making new lows. As long as we can maintain current levels or get back to $50 a barrel, central banks are headed towards a huge overshoot of inflation.

Recent Comments