April

02

April

02

Tags

Euro Vulnerable to ECB Rhetoric

Heading into the ECB meeting this month, FX markets have witnessed significantly different price action than the run up into the prior two meetings. This time around speculators appear to have much less appetite to step in front of the ECB and place bets on easing of monetary policy. Price action before and after the last two European Central Bank gatherings offered clues on short term market positioning.

In February, the EUR weakened going into the policy meeting. Most of the weakness came on German CPI numbers and the Euro continued to decline as Flash Eurozone CPI was released later that week. Markets were disappointed in February when the ECB introduced no new policy measures. Draghi pointed towards March when more information would be available, specifically the ECB’s quarterly projections as well as additional information on Q4 2013 GDP.

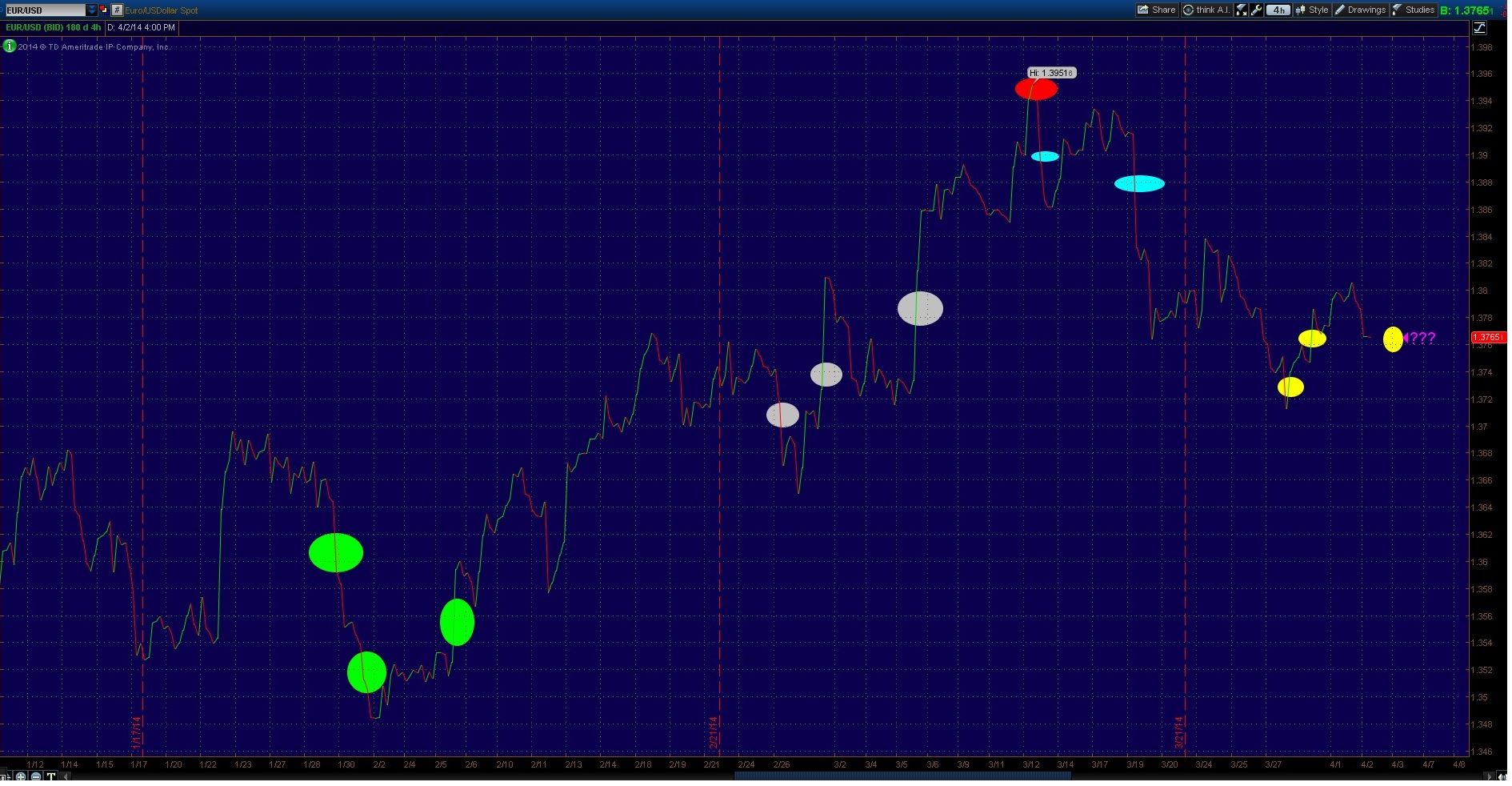

As seen below, the series of green circles from left to right show the succession of events with the German CPI on the far left, Flash Eurozone CPI in the middle green circle and lastly the February 5th ECB meeting. The ECB’s decision to remain on hold caught shorts wrong footed and the EUR continued to rally for the rest of the month.

EURUSD 4HR Line Chart 6:59pm 4/2/2014

The ECB’s staff projections were released at the March meeting, but there was still no action. Seen in the white circles on the chart, the EUR sold off on the German CPI release in early March. Later that same week shorts were squeezed as the Flash Eurozone number came out above expectations as French prices helped wider Euro area inflation. The March 6th ECB press conference heard a classically calm Draghi speak about how the Eurozone was an “island of stability”. He explained away most of the concern for low inflation as related to food and energy, and necessary rebalancing of periphery economies. The March ECB meeting is highlighted in the far right white circle. From March 6th the EUR rallied for the following two weeks towards the 2014 high near 1.3950.

On March 25th as EURUSD approached 1.3950, Draghi made a comment regarding the exchange rate becoming significantly more important in the ECB’s analysis of its low inflation problem. This event is highlighted on the chart in the red circle. The EUR has remained under pressure since this speech, helped by a stronger dollar on the back of a better than estimated February Jobs report and a more hawkish than expected Janet Yellen at her first press conference. These events are labeled in the blue circles. The April ECB meeting is less than 24 hours away and there are significantly lower expectations this time around. The EUR has not sold off prior to the meeting, and money market rates are not pricing in any action. The FT reports that markets broadly expect a dovish tone but no action.

The FT reports:

A poll by Reuters found 18 of 22 money market traders thought the European Central Bank would not change policy at its meeting on Thursday.

Another survey conducted last week by the wire service saw only two of 72 economists arguing the central bank should take action.

The tone of everything I have read in the past three days seems to be in unanimous alignment that no action will be taken. This seems to be pretty much the opposite of EUR sentiment prior to the last two meeting when easing bets were harshly squeezed once there was no new policy announced. This time around it seems less dangerous to have a short bias as expectations are much lower. Ironically the most recent data released in the last few days have shown German inflation, Flash Eurozone CPI and Eurozone PPI all to be at the lowest levels in recent months.

March Flash Eurozone CPI(Eurostat):

Mario Draghi has shrugged off inflation as mostly driven by food and energy prices, which is seen in the table above. Reading more into his March 25th comment, Draghi seems more willing to admit that a large driver of the decline in energy and food prices is due to a rising exchange rate. Draghi regularly refers to “prevailing energy futures prices” in his assessment of inflation. The specified futures contracts are priced in US Dollars, therefore a rising EUR is driving energy and to a lesser extent food prices lower. On Thursday it may not take any easing action to send the EUR lower. In February 2013 the ECB adjusted the statement to include a new piece of language referring to the exchange rate:

“Risks to the outlook for price developments continue to be seen as broadly balanced over the medium term, with upside risks relating to higher administered prices and indirect taxes, as well as higher oil prices, and downside risks stemming from weaker economic activity and, more recently, the appreciation of the euro exchange rate.“

The adjustment to the statement marked the top for the EUR rally in the first half of 2013. On a medium term outlook, Thursday and Friday provide a significant opportunity for a prominent sentiment turn for EURUSD. A more dovish than expected ECB along with a non farm payrolls report higher than estimated should be enough to turn the trend.

Pingback: Draghi Talks QE | Trenders Game