January

07

January

07

Draghi Stares Down the Ultimate Question On January 22nd

After three years of an impeccable but relatively untested performance as President of the European Central Bank, Mario Draghi has finally backed himself into an inescapable corner. Global markets are now hinged on what over 90% of banks polled say is a imminent move to buy massive amounts of sovereign Eurozone bonds that will come at the next ECB meeting on January 22nd. Obviously size is a key issue, and markets would probably need 500-750bn EUR to consider the program legitimate.

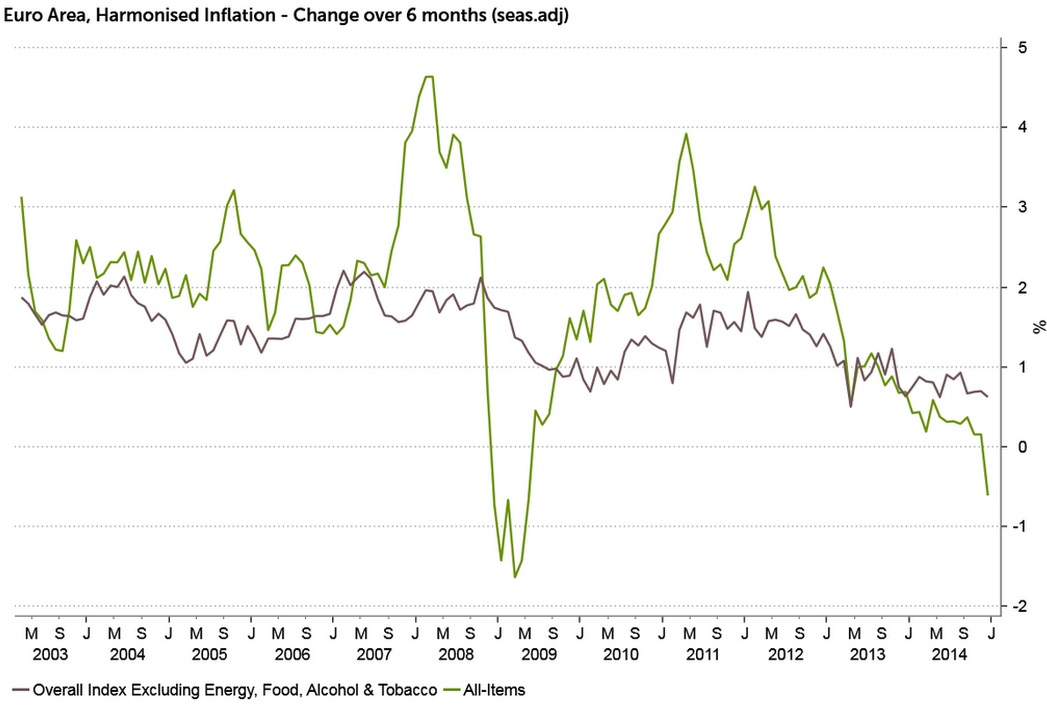

The last ECB meeting saw a split governing council, as 6 out of 24 members opposed the change in language that the ECB now “intends” to meet their balance sheet target rather than “expecting”. This change in the statement was seen as implying an open door to sovereign bond buying. ECB Vice President Constancio also commented last month that Q1 2015 would be the time to make a decision government bond buying program. Ironically Jens Weidmann’s gang of hawks may actually be emboldened by today’s inflation data. Eurozone inflation numbers showed that overall prices fell -0.2% year over year, while estimates were for an unchanged 0.0%. The EUR traded choppily lower a few pips as headlines read “Europe falls into deflation”, but EUR was likely supported by the core inflation reading of 0.8% against expectations of 0.6%. Core inflation has remained very stable for the last year, with oil representing almost all of the decline in CPI.

Even if hawks on the ECB’s governing council are in the minority, they would have a valid case that it’s unwise to launch a controversial massive government bond buying program simply because of a unique one time plunge in oil prices. Deflation is not a concern when you look at the core readings on prices. These declines in CPI will roll out of the year over year readings within 8 months anyway, putting you right back to 1% headline CPI.

I believe too much has been made of Draghi’s now weekly comments on how the ECB is missing it’s mandate. The ECB president already has a reputation as a secretive leader that says things the governing council didn’t agree to, most notably his words at Jackson Hole that initially started the markets obsession over ECB QE. Markets take Draghi’s words as “QE hints” when they are actually just a man building a case for a policy he doesn’t have ample support for. Draghi may be able to push through a QE program, but the size of the program is now obviously the sticking point that has the largest potential to backfire if the program is seen as too small. The banks piecemeal slow motion approach to easing just doesn’t seem to bode well for current market expectations of a “bazooka” program, that is ultimately unlikely without German support.

Three dates over the next month provide a critical turning point window in Euro sentiment (and everything else). The European Court of Justice will make public it’s opinion of ECB government bond purchases on January 14th. Last year the German high court referred the ruling on the decision to the ECJ in an attempt to pass the responsibility on to the highest Eurozone judicial body. This decision is seen as the judicial ruling on “Whatever it takes”. Obviously the ECB meeting is on January 22nd, with the Greek election three days later on January 25th.

It is impossible to anticipate the outcome of any of these events, but given the large short Euro position the market is currently holding it seems wise to view this as a possible medium term (3 months) turning point in sentiment. Our views on factors supporting the USD are also turning less optimistic, we conclude that EURUSD is a great target for a contrarian approach for Q1 2015.

Recent Comments