April

04

April

04

US Economy in Flux

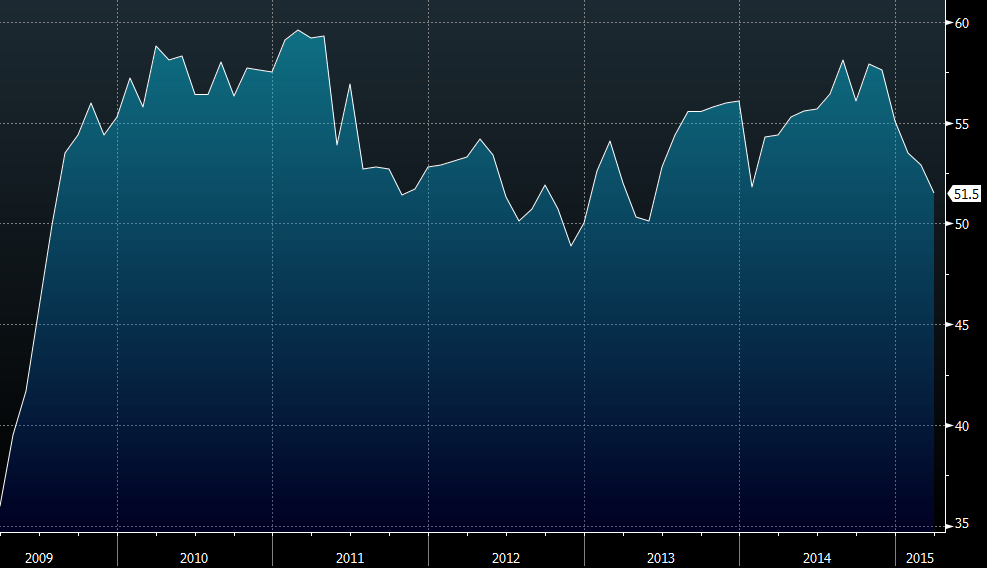

The Dollar fell late last week as two key data points showed that the US economy is losing steam. ISM manufacturing data came out at 51.5 which is the lowest level since Spring 2013. The survery missed estimates of 52.5 and is now only slightly above contraction territory. Payrolls were also very disappointing, with only 126k jobs being created in March versus estimates of 240k. There were also cumulative downward revisions of 69k to the two previous monthly reports.

These two economic indicators cap off a string of worse than expected data that also includes retail sales and durable goods orders. All top tier economic indicators have turned lower since the start of the year. Some have laid the blame on weather, but I think it would be incorrect to compare this Winter’s weather slowdown to last year. The 2014 Polar vortex was truly a black swan type weather event, with large portions of the midwest and northeast experiencing huge amounts of snow and temperatures far below zero. That has not been the case this season, as most of the bad weather was isolated to the Boston area.

The West Coast ports strike has also rightly shouldered some of the blame, but I am surprised at the extent various financial media outlets have for the most part dismissed the possibility that the economy is simply once again slowing down right when consensus said it was taking off. The strong Dollar and fall in oil prices is obviously having a large impact as mining jobs fell sharply for the second straight month, durable goods orders declined sharply and various regional manufacturing sentiment surveys have seen large declines even in areas where the weather was normal.

The worst of the weather and West coast ports strike occurred over a month ago, so it doesn’t really make sense that the data is now taking yet another leg down suddenly. The broad nature of the slowdown, and consistently bad numbers for three months now tells me that there is something larger at work here. It is possible that the great slowdown in the oil industry is finally reaching all corners of the economy, and the strong dollar is only making it worse. Looking into some of the graphs below, the fact that expectations of future growth are also plunging doesn’t really support the argument of short term factors driving the current weakness.

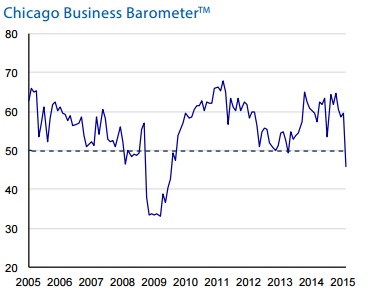

Chicago PMI

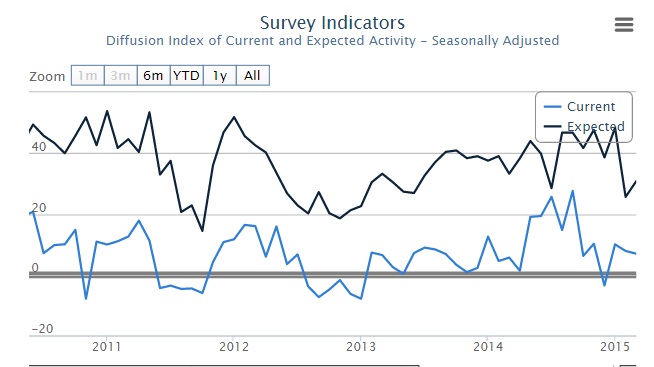

Empire(New York) PMI

Monthly Change In Goods Producing Jobs

ISM Manufacturing PMI

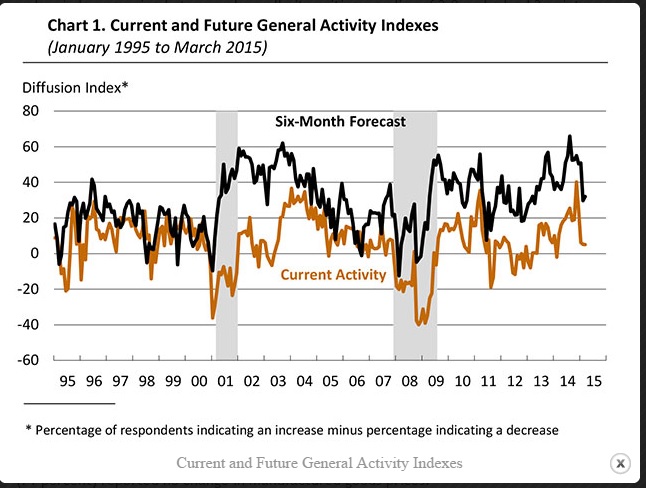

Philly Fed PMI

The question for currency traders is how does this affect the US Dollar going forward. The FOMC needs to see proof of inflation on the way to 2% and sustained strength in the labor market before raising interest rates. The likelihood of these two things happening seems to be becoming less and less likely, which is something Dollar bulls will surely take note of next week once everyone is back in the office from Easter weekend. USD longs remain a very consensus trade, with positioning still near the highest levels on record.

I will be watching US stocks closely. Investors may finally decide that the historically rich valuation of 17 times forward earnings for the S&P 500 is simply too high given the significant downward revisions in earnings since the start of the year. The strong dollar, weak oil price and subsequent slowdown in the broader US economy will eventually weigh on equities. The Dollar and equities have been correlated for much of the last several months, meaning that if stocks crack then so will the Dollar. Keep an eye out for USDJPY taking a big leg lower, especially in case of continued uncertainty over Greece’s bailout program.

Recent Comments