May

05

May

05

Big Boys Sellin’ Bonds

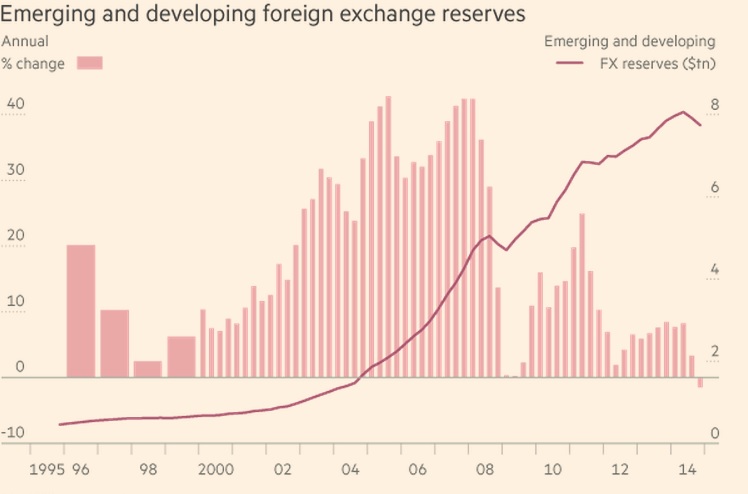

There have been a flurry of articles over the last month about emerging market economies beginning to drawdown their FX Reserves. Foreign exchange reserves serve as a rainy day fund: assets accumulated by exporting economies that implement some form of currency peg(manipulation). China is the main user of this strategy, building up a $4 trillion dollar war chest since the Yuan was pegged to the Dollar in the mid 1990s. The oil exporters joined the FX reserves party in the 2000s as oil broke above $20 a barrel leaving countries like Saudi Arabia with huge windfall profits, helping them build up nearly $1 trillion dollars since 2000. This “big boy” buying of fixed income assets was seen as one of the main causes of the mid 2000s housing bubble as sovereign wealth funds piled into mortgage backed securities which were seen as very safe assets indirectly backed by the US government.

These funds are now starting to sell their bonds in significant size, squaring off against the global central banks in a bond market showdown. Saudi Arabia has drawn down by $36bn or 5% of its reserves in the last two months, $20bn in March and $16bn in February. China releases FX reserves data quarterly, drawing down $113bn in Q1 2015 to a total of $3.73tn remaining. China sold off $44.7bn in Q4 2014 and $105bn Q3 2014. Averaging out the last couple of months would imply that around $56bn per month in sovereign bonds is being sold per month by these two players. The IMF collected data for January and February of 2015, stating that the total drawdown across all EM economies was $300bn for the two month period.

With central banks buying around $131bn per month, the effect of sovereign wealth funds selling is obviously muted in a big way. For now, the total asset purchases by global central banks is around equal to the amount of bonds being sold by exporting nations. It is impossible to guess what exactly would be happening in the bond market if the various QE programs were not underway, but the huge jump in bund yields over the last week gives us an idea. Now that sovereign wealth funds are a source of steady supply, if speculators join in the party and get squeezed on a heavily crowded position we see that yields can jump very rapidly. This entire scenario is exacerbated by the fact that liquidity is rapidly declining in the global bond and rates markets. This last week’s surge in core Eurozone yields could have been linked to China’s April 20th announcement that they were drawing down $60bn for the purpose of injecting much needed funds into state owned banks.

Most FX reserves are generally around 2/3rds in US dollars according to the IMF. With the runner up being the Euro at about 15-20%. Sterling and Yen make up the remainder. This distribution of funds is what drives the seemingly coordinated moves in global sovereign rates, as sizable FX reserves are drawn down all developed market yields rise in tandem.

I have to note that the first two months of the year were when the oil bear market reached its lowest levels so far, much of the selling FX reserves came from high cost oil exporters like Russia, Venezuela and Nigeria. Throughout February much was made of the steep falls in Russian FX reserves, declining at around $6bn per week. The point being that the longer oil stays depressed, the faster oil exporters will blow through their savings. In China, the more the economy slides the more Xi has to drawdown FX reserves to defend the currency and keep banks capitalized.

Recent Comments