October

11

October

11

Can Wynn Resorts Buck The China Bears?

The four US traded Macau Casino operators: Wynn Resorts(WYNN), Las Vegas Sands(LVS), MGM Resorts(MGM) and Melco Crown Entertainment(MPEL) have rallied sharply in the last two weeks as shorts were squeezed across a range of China related stocks. Macau casino betting peaked in Spring 2014 and has been sliding ever since. These companies have seen their share prices decimated by 50%-70% over the last year as a President Xi Jinping’s corruption crackdown and slowing economic growth have seen gross gaming revenue fall 33% year over year as of September 2015.

As of Q2 2015 Wynn Resorts receives 60% of its revenue from Macau, a number that could rise as high as 75% when Wynn Palace opens in March 2016. The stock price traded down to a low near $51 per share in late August as a swirl of negative sentiment surrounded China stocks and Wynn Macau junket operators were the victims of a $13 million employee orchestrated embezzlement scam. Junkets in Macau are an element of the shadow banking system, lending billions of Dollars worth of credit to VIP gamblers that are Wynn’s bread and butter.

The embezzlement scandal only focused more attention on the shadowy world of Macau money laundering and currency smuggling. It has become clear that the former Portuguese colony is now being used by China’s top businessmen and communist party members to get Yuan converted to other currencies and out of China permanently. This presents Macau operators with a huge challenge of abruptly changing business models from catering to (corrupt) Chinese VIPs to now focusing on the ‘regular’ middle class gamblers.

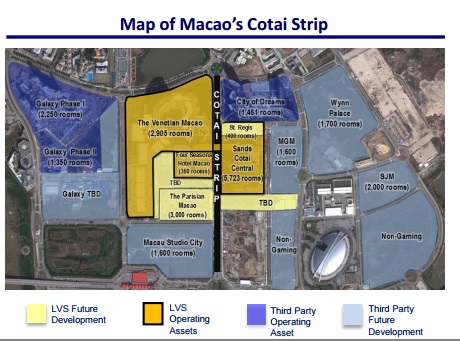

Las Vegas Sands is best poised to weather this storm as the company nearly single handedly built the Cotai strip and operates thousands of hotel rooms there already. Wynn has no Cotai presence at the moment, as the Wynn Macau complex is on the Macau peninsula several miles away from Cotai. This however is what offers Wynn the most growth potential, Wynn Palace’s 1,700 rooms will finally earn them a piece of the mass market Vegas style Cotai strip district. Wynn and MGM are the only remaining licensed US operators without a property there, both already having built enormously profitable casinos in the dense populated city peninsula.

Wynn’s $7.7 billion market cap makes it the smallest player in the space by far. It is also extremely leveraged with an 8 times debt to equity ratio while Melco and Las Vegas Sands have Debt to Equity ratios of 1x. These factors make the stock very volatile, but offer a small base to work from which means EBITDA could nearly double as soon as the doors open at Wynn Palace. Forward valuations for 2016 have dropped precipitously along with share prices, with Enterprise Value/EBITDA at 7.25x for Wynn, 10x for LVS and 10x for Melco Crown. I assume the massive leverage Wynn employs discounts the valuation.

The tail risk for all of these companies, beyond the Chinese macro situation, is their USD functional parent companies all have massive inherent currency exposure. The declines that hit the sector in late September started just after the PBOC devalued the Yuan. If there is more Yuan devaluation to come, these casino operators could face insurmountable headwinds as the government finally pulls the rug out from under them. Las Vegas Sands’ earnings report will tell us everything we need to know about Q3 Macau performance and they are the first to report from the sector, coming out next week.

Recent Comments