April

22

April

22

Clock Ticks on China Sentiment

AUD, NZD and EM(ZAR,TRY,MXN) currencies have had a strong 8 weeks. Ironically this strength seems to have been helped by slowing data from China. The worse the numbers have come out the more the market seems to expect a bold stimulus program, but these hopes have been all but dashed in the past week. The Chinese government seems content with shortening the timeline of existing public works and infrastructure projects, but is offering no new blunt monetary easing. China related currencies have traded lower or flat in the past three or four sessions.

Sentiment on China has coasted for the past two months as the markets seemed to be driven by two factors. Selling Dollars to fund carry trades in EM currencies that were relatively cheap after January’s rout. I have covered why some of this USD selling may have actually been China itself. Secondly there were hopes in the wake of last month’s HSBC China Manufacturing PMI miss that the data was so bad that there had to be a stimulus. We now know that is not the case, the bar for new easing is high.

The data out of the world’s second largest economy has slowed significantly during the post Yuan intervention period, I mark this era as starting on February 24th 2014. I have written on why a falling Yuan is a huge threat to China’s economy, and the world. The unwinding of USDCNY carry trades has already started to reduce credit in the Chinese economy. Total social financing (broadest measure of lending) fell $90bn (9.9%) year over year in the first quarter as the spigot of cheap dollars was cut off by the explosion in fx rate volatility. New trust loans, a favored source of financing for developers, fell 78% YoY in Q1.

There has also been a flood of articles out from the FT, WSJ and Economist over the past 7 to 10 days elaborating on just how bad the situation is. While none of these developments are particularly new, the circumstances are pretty grim and will be exacerbated by the Yuan selloff. To sum up, there is a huge oversupply of homes in tier 2 and tier 3 cities and prices are starting to fall. Developers are in a cash crunch because they can’t sell the apartments to finance their debt. Many of these developers have issued large amounts of dollar denominated bonds in the past 2 years, which creates significant FX risks from the recent move higher in USDCNY. Another financing source for developers has been the shadow banking system, specifically wealth management products and trust loans that up until February were awash with carry trade cash eager to be invested in real estate. To make matters worse, a special report in the Economist this week stated that local governments in china get upwards of 60% of their revenue from seizing land and selling it to developers. The term Ponzi scheme does come to mind in summarizing all this…

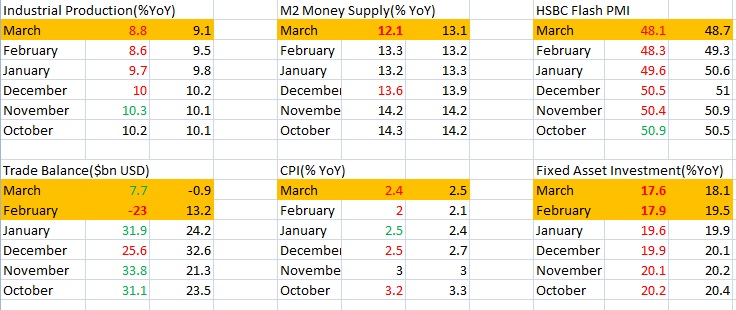

The China bearish case is not a new idea, but the effects of the Yuan intervention that began February 24th are yet to be seen. Below is a before and after of recent data. Orange highlighted data has been reported during the intervention period:

I would focus most of my attention on M2 and inflation. The money supply has contracted as carry trade money dries up. Inflation is rising as imports like food and energy have grown in cost as the Yuan has fallen. The ruling party is in a tough situation where they have to keep inflation up, but the only way to do it is by devaluing the Yuan, because China’s monetary policy is for the most part in the hands of the Federal Reserve due to their currency manipulation policy. Devaluing the Yuan brings about its own massive set of risks that will play out over the next few months. AUD,NZD,ZAR and TRY are likely to be vulnerable to a shift in sentiment.

Recent Comments