April

30

April

30

EURO: 99 Problems

The Euro is starting to look very vulnerable in the wake of recent data on inflation and money growth. Additionally short term interbank rates are on the rise, meanwhile periphery bond spreads have plunged to multi year lows. In the past four months, Ireland, Portugal and Greece have all returned to capital markets and have sold bonds at yields that would imply the European debt crisis has completely abated. On the economic growth side, the recent purchasing manager sentiment indexes have been positive showing that growth is still continuing at a moderate pace. While these positive releases on economic sentiment show that the Eurozone recovery is proceeding, the decline in prices and the money supply are a significant threat.

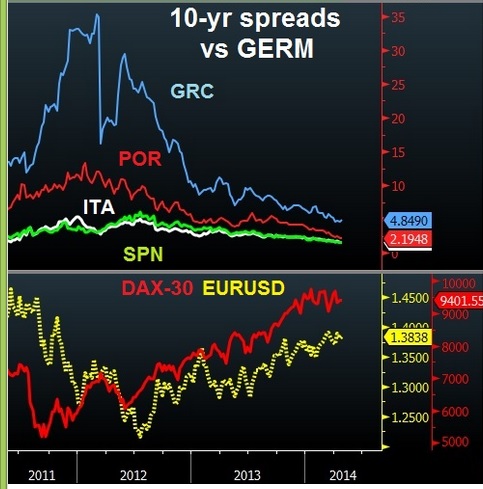

Periphery Debt Overvalued-

Market pundits seem to believe that Draghi’s July 2012 promise to do “Whatever it Takes to save the Euro” was the catalyst that fixed the Euro crisis. It is debatable whether Draghi actually fixed anything, even though he loves to pat himself on the back for saving the day. Nearly 3 trillion dollars in monetary expansion has been undertaken by the Fed, BOJ and PBoC over the last 18 months that stormed into Eurozone bond markets and sparked a massive rally in periphery debt. Relative to US government bonds, there is not much value left in periphery debt and these assets could already be fairly valued.

Given this dynamic of external easing fueling out performance in periphery stocks and bonds, the Eurozone is particularly vulnerable to a global tightening in credit. Countries like France and Italy that have lagged in their reforms, and still rely heavily on external capital are especially exposed. Central banks are already reducing the size or pace of balance sheet growth as the Fed slows QE, LTRO loans are repaid and China FX reserve growth slows (Chinese banks are also reducing lending to risky countries).

Rising Money Market Rates-

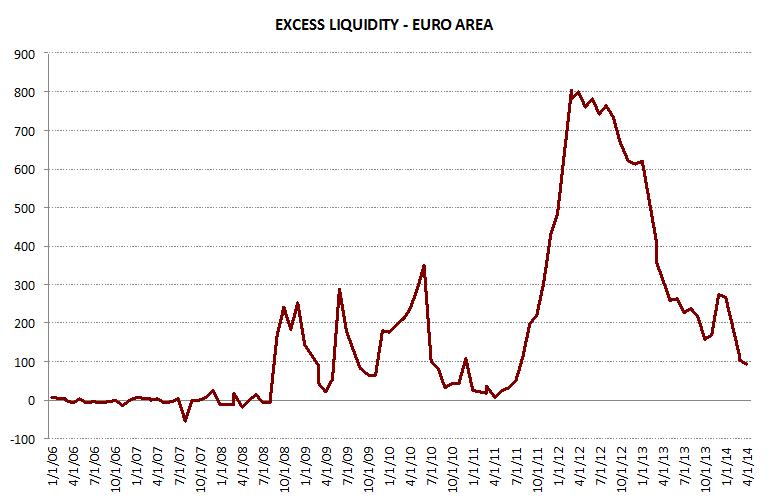

The issues Mario Draghi has harped on repeatedly this year are a prolonged period of low inflation and an unwarranted rise in money market rates. Overnight money market rates have been on the rise over the past two weeks as seen below. This rise in overnight lending is especially harmful to periphery banks that are more likely to be funding themselves on a short overnight basis. As banks repay LTRO loans, excess liquidity in the Eurosystem has fallen below the important psychological mark of 100bn.

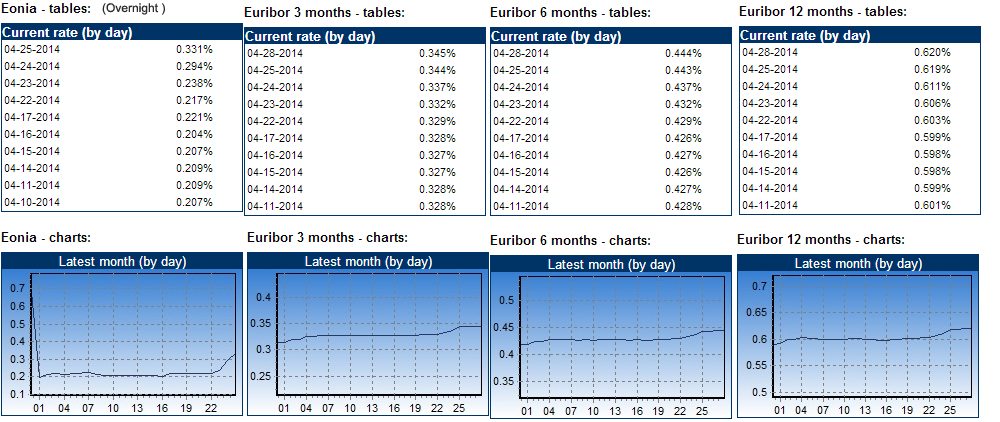

EONIA(overnight lending rate) has fixed above the ECB’s overnight cash rate of 0.25% several times in the past week, which represents a clear malfunction in transmission of the ECB’s policy. Mr.Draghi also likes to pat himself on the back for the ECB’s genius forward guidance not allowing short tenor money market volatility to propagate down the interest rate curve to the 1 year rate. I am guessing that self congratulating session won’t be going on at next week’s meeting as for the first time in months longer tenor Euribor rates are starting to tick up. 3 ,6 and 12 month rates have been on the rise during the last 2 weeks of the entire curve moving higher, lead by sharp moves up in EONIA. See the graph below:

Low Inflation-

This morning’s Flash CPI estimate missed expectations at 0.7% vs 0.8% expected. Low inflation continues and the pressure is building on the ECB to ease policy. The central bank has attributed much of the decline in inflation to falling food and energy prices, however the caveat here is that those items (commodities bought on futures exchanges) are mostly priced in US dollars. The rising EUR is the culprit behind falling energy and food prices, and rightfully so Draghi is becoming more willing to blame the inflation problem on the strong exchange rate. The Eurozone is also the most vulnerable victim of China’s new policy of exporting deflation by devaluing the Yuan. The Chinese currency has fallen around 3% since February, which is surely having an effect on import prices in the Euro area as seen by German import prices since March. Contracting lending and rising money market rates also will feed through into lower inflation and a tighter money supply.

Contracting Lending –

Private loan growth continues to bump along near recent lows as Euro zone banks reel back lending in the face of ECB stress tests that will begin next month. Draghi has personally attributed the fall in lending to banks changing their behavior as they clean up their balance sheets in anticipation of the Asset Quality Review (stress test.) It is possible that the ECB sees this fall in lending as a temporary side effect of such a stringent analysis of bank assets. Contractions in lending are also due to a post crisis decline in asset backed loan securitization, something that the ECB has discussed extensively.

Overall the Eurozone has a plethora of problems. Mario Draghi can ease policy based on any of the usual suspects, low inflation, unwarranted rises in money market rates or contracting lending. While these are all significant issues in their own right, the main issue here is that the Eurozone has effectively been the biggest beneficiary of the unprecedented amount of monetary easing that has occurred since late 2012. The gains in periphery bond markets have boosted confidence in those economies, and helped banks repair their balance sheets. As the Fed reduces QE, the PBoC FX reserve accumulation slows, LTROs are fully repaid and the Bank of Japan waffles on increasing its QE…. the Eurozone periphery bond market stands to be the most vulnerable and overvalued asset in the game. The ECB now needs to implement its own easing program, up until now everyone else has done the heavy lifting for them.

{kind=link}

Recent Comments