May

05

May

05

Market Bets Yellen Sleeps on Good News

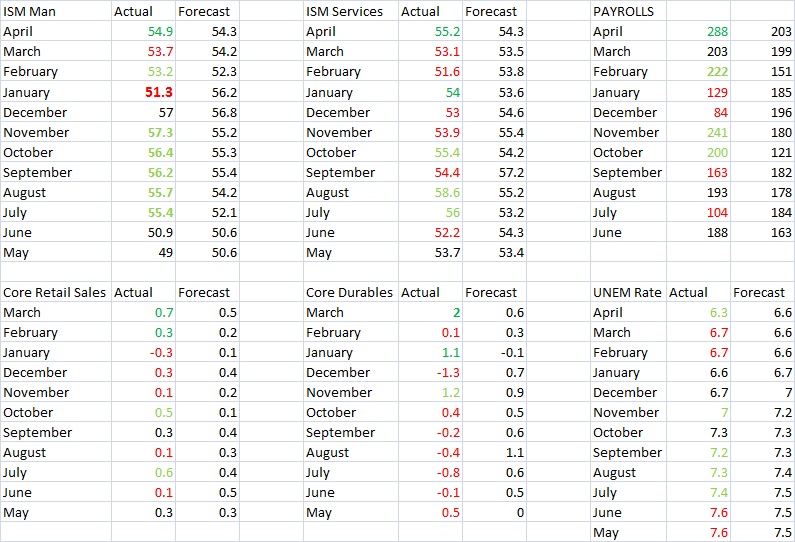

Friday was a frustrating day for US Dollar bulls and bond market bears. The non farm payrolls data showed that 288k jobs were created, while the unemployment rate fell from 6.7% to 6.3% . On the flip side, wage growth fell from 2.0% to 1.9% year over year. Additionally much attention was given to the sharp decline in the labor force participation rate that fell from 63.2% to 62.8% as 806,000 Americans dropped out of the labor force. It is strange so much focus was placed on the labor force participation rate as it only declined to October 2013’s level. Also Janet Yellen herself said in February 2014 that “I think a significant part of the decline in labor force participation is structural and not cyclical”. (The Philly Fed wrote an interesting paper on this topic)

In the wake of the data release, the US Dollar and US government bond yields surged higher. An hour later both had given back all their gains and closed near the lows of the day. Reading through interpretations of the WSJ, FT and other market reporters it seems that the market sentiment is that Friday’s data will not change the Federal Reserve’s schedule for tapering or rate hikes. It appears that the FOMC has run so many fire fighting operations, that the market no longer believes that can ever produce and stand by a hawkish utterance.

Looking back over the data released in the past month, its becoming hard to believe markets are stuck in these ranges. Nearly every top tier indicator has beat expectations. First quarter GDP was a disappointment (consumption was steady), and New home sales missed expectations(pending homes sales beat). Excluding these two data points, recent US economic performance has been very good.

Given the collection of data currently at the FOMC’s disposal, Yellen’s speech on Wednesday will be closely watched. The original purpose of QE3 was to reduce labor market slack and they have been successful at that goal. Unfortunately, the FOMC has developed a habit of moving the goal posts or switching the focus to inflation, wage growth or labor force participation.

After being conditioned to expect suppression of volatility, traders see a slim glimmer of hope that the Fed has the courage to take a stand and force a small adjustment in short term interest rate markets. As US data improves it becomes more irresponsible for the FOMC to let the two year yield (among other rates) drift along at 0.40%. If Yellen makes it a point to talk up labor market improvement or mention recent increases in CPI/PPI this week there may be a chance for a rally in the US Dollar.

Recent Comments